Public finance tax lawyers have been acutely aware of the direct effects of the 2017 tax legislation, especially the elimination of tax-exempt advance refundings, but some of the indirect effects have begun to appear only recently. One of those is the triggering of bank rate adjustments resulting from the drop in the corporate tax rate. As frequently touted by the President, the legislation reduced the maximum corporate tax rate from 35% to 21%. The effect of this rate reduction on bond interest rates is more pronounced because of the popularity of bank placements of tax-exempt bonds in recent years. For a number of reasons, including to remain competitive, many banks have been willing to forego or reduce the interest rate increase to which they are entitled under the bank loan documents. This is obviously good news for bond obligors but the tax consequences – namely, a potential reissuance – must be kept in mind.

One of the early reissuance authorities – Rev. Rul. 87-19 (available here) – first articulated the proposition that a bank’s waiver of an automatic interest rate adjustment resulting from a change in the maximum corporate tax rate is treated as a change in the interest rate that might trigger a reissuance.[1] While on a superficial level it might seem counterintuitive that a non-change in interest rate would cause a reissuance, the IRS correctly recognized that the non-change, which results from a modification of the agreement between the bank and the obligor, is the sort of change that, if sufficiently material, will cause a reissuance. Rev. Rul. 87-19 predated the “Cottage Savings” regulations, i.e., Reg. 1.1001-3, which have since established that a change in interest rate greater than 25 basis points (0.25%) or 5% of the original rate, whichever is greater, will cause a reissuance.

The interest rate adjustment described above results from a provision in many bank loan documents that is based on the maximum corporate income tax rate. The underlying rationale is to keep the bank whole in the case of a corporate tax rate reduction because such a reduction reduces the bank’s “taxable equivalent yield” of the tax-exempt rate. For example, at a 35% corporate tax rate, a 5% interest rate on a tax-exempt obligation has a taxable equivalent yield of 7.69% (0.05/(1-0.35)), because that rate reduced by a 35% tax is 5%. At a 21% corporate tax rate, the taxable equivalent yield of that 5% rate is only 6.33% (0.05/(1-0.21)).

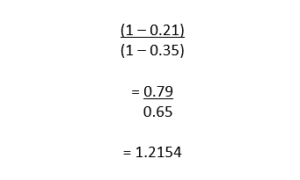

The rate adjustment, sometimes referred to as a “margin rate factor,” can be expressed as (one minus the new maximum federal corporate tax rate) divided by (1 minus the prior maximum federal corporate tax rate). In the case of the recent change in the federal corporate tax rate, the factor would be:

With an original interest rate of 5%, the adjusted rate resulting from the recent tax legislation would be 6.0769% (0.05 * 1.2154). Thus if the adjustment were waived and the interest rate remained at 5%, the “change” in rate would be 1.0769% (6.0769% – 5.0000%), and a reissuance would result from the waiver because the change is greater than 0.25%. Some banks will waive the adjustment only in part, in which case the new rate must be compared to what the rate would have been with the contractual adjustment. The difference between those rates is compared to the 25 basis point threshold to determine whether a reissuance has occurred.

As is likely apparent, the higher the pre-adjustment interest rate, the more likely a reissuance will occur. In fact, for any pre-adjustment interest rate above 1.1607%, a full waiver of the interest rate adjustment described above will exceed the 0.25% threshold and cause a reissuance. Given the low interest rate that will trigger the reissuance, the close calls will involve partial waivers, waivers with respect to very short maturities (e.g., if the bank-held bonds have varying maturities) and variable rate bonds.

Generally, a reissuance does not cause a problem as long as it is recognized and treated as a current refunding. Thus it will likely require a diligence review, tax certificate and Form 8038(-G) filing. While there is always a change in law risk, that risk generally has not been a problem (particularly after we dodged a bullet when the House proposal to eliminate tax-exempt private activity bonds in the 2017 tax legislation was rejected).

[1] If the interest rate is adjusted at the option of the holder, rather than an automatic adjustment, failure to exercise the option would not cause a reissuance pursuant to Regulations 1.1001-3(c)(3) and 1.1001-3(c)(5) (see also Example 9).