Remedial actions, the IRS Voluntary Closing Agreement Program, and IRS audits – these are the three venues in which most problems with tax-exempt bonds are aired. We’ll ignore remedial actions in this post (as well as most rebate/yield reduction payment problems). We’ll focus instead on the IRS Voluntary Closing Agreement Program (usually abbreviated as “VCAP”) and audits.

Although VCAP and IRS audits are different in some respects, they often converge on the same point – a closing agreement with the IRS that preserves the tax-advantaged status of the bonds. The IRS usually will agree to a closing agreement only if the issuer agrees to redeem some or all of the bonds and agrees to cut a check to the IRS. We’ll ignore the bond redemption point in this post. We’ll focus instead on how to figure out how big the check will be.

For tax-exempt bonds, the “closing agreement amount” is often based on the “taxpayer exposure” on the bonds.

The guidance from the IRS on how to calculate the “closing agreement amount” for a VCAP or an audit makes it sound very mechanical – fire up Excel, walk through the steps, hit enter, and out comes your bill. But – put your coffee down for a second – the process is actually much more dynamic than that. In many cases, the issuer will want to weigh its strategic options in how it presents a VCAP request and makes an opening offer, or how it negotiates in an audit based on the likely closing agreement amount that will result. For example, if the issuer wants to sell a bond-financed building to a private user, and no remedial action is available, then the likely closing agreement amount in VCAP may be a critical detail.

The provisions in the Internal Revenue Manual that relate to VCAP closing agreements, which the IRS recently revised, contain many “standardized” terms for certain common “identified violations.” Finding your violation among the “identified violations” simplifies matters, but it only gets you so far. Most of the identified violations require further calculations, and many of them are based on some percentage of “taxpayer exposure,” even if it is only “taxpayer exposure” on a smaller subset of the bond issue. Similarly, in an audit of tax-exempt bonds, the closing agreement amount is almost always based on taxpayer exposure, albeit more likely on all of the outstanding bonds of the issue.

“Taxpayer exposure” is designed to compensate the IRS for the revenue it lost when it didn’t collect tax on the interest on bonds that purported to be tax-exempt bonds, but which were actually taxable bonds.

As we said before, the concept of “taxpayer exposure” makes perfect sense – you thought you had tax-exempt bonds, so the bondholders didn’t pay tax on interest on the bonds. But the bonds didn’t meet all the tax requirements, so interest on the bonds was actually taxable. “Taxpayer exposure” is designed to make the IRS whole for that uncollected tax.

Because bondholders generally get a three-year statute of limitations on their tax return, the “taxpayer exposure” also generally will be limited to interest during the three years prior to the year of the violation (more on this later), but the statute of limitations operates based on the assumption that the tax due in a given year is not paid until the April 15th filing deadline the year after. Because the taxpayer exposure calculation for the bond issue ties back into the bondholders’ tax returns, you can’t just add up the interest on the bonds in the current year and the two prior years (for a total of three years), figure out the tax on that interest, and call it a day.

The steps to calculate taxpayer exposure are in Internal Revenue Manual section 4.81.6.5.3.1. Feel free to read through the language, but we’ll talk through the steps below.

Step 1 – How far back do we have to go? (Resist the temptation to just count the interest in the current year and the two prior years.)

The first question is – how many prior years of interest do we have to include? It’s a matter of picking a key date and then counting backwards. The key date in VCAP is the date that the issuer submits the closing agreement request. The key date in an audit is the date that the IRS sends written notification to the issuer that it has identified a compliance failure for the bonds. (Ok, fine, we’ll call it the “Key Date.”) Once you’ve picked that date, count backwards on the calendar to the first April 15th that you encounter. That April 15th that you just encountered is the due date for the tax return for the immediately prior year. That prior year, and the two years that precede that prior year, are the prior years for which interest must be included.

The rule of thumb is this: if the Key Date is past April 15th, then the immediately preceding three calendar years are the applicable years. If the Key Date is before April 15th, then the immediately preceding four years are the applicable years.

If the IRS determines that the issuer didn’t proceed in good faith, they can require the issuer to look back six years (under the same rules above), instead of three.

Step 1, part 2 – How far forward do we have to go? All interest that accrues on the bonds from the Key Date through the date that the bonds are all redeemed is included in the calculation. And yes, redeemed means actually redeemed, and not merely defeased.

Step 2 – Add up the interest in a year. Pretty simple. One annoying aspect of this is that you often have to carve up the interest payment schedule for the bonds into calendar year sections, unless the interest payment schedule is unusually detailed.

Step 3 – Multiply each annual interest amount by the “relevant tax percentage.” This step mimics the IRS taxing the interest on the bonds that should’ve been taxed. Until further notice, this rate is 29%. 29% is intended to be a rough approximation of the average bondholder’s effective federal income tax rate.

Step 4 – Adjust the time-value of each of these payments forward or backward to the closing agreement date, or, “the counting of the April 15ths.” First, treat the amounts from Step 3 in each year as having been paid on the following April 15th. (In effect, you’re mimicking the filing and payment of tax on the interest on the bonds in that year, which would have occurred when bondholders filed their tax returns on the following April 15th.) For any of these deemed April 15th payments that are before the closing agreement date, you must future value them forward to the closing agreement date. For any of these deemed April 15th payments that are after the closing agreement date, you must present value them back to the closing agreement date.

This step is often the trickiest when you’re calculating taxpayer exposure for planning/strategy purposes, because you have to estimate when you think a closing agreement will be reached with the IRS, which is a very inexact science. Thankfully, the inherent nature of the present/future value calculations means that a difference of a few months here or there won’t cause wild swings in the closing agreement amount.

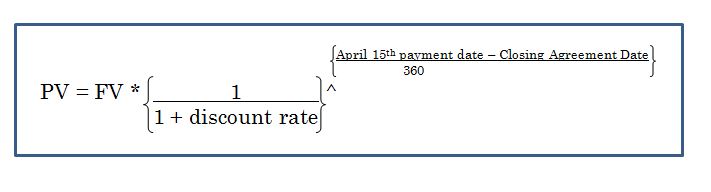

To future value the deemed April 15th payments that come before the closing agreement date forward to the closing agreement date, use the applicable underpayment rate under Code Section 6621 (which has been 3% for several years now) as the discount rate and a daily compounding methodology. Note that the applicable underpayment rate is not the same thing as the “Applicable Federal Rate” (or “AFR”). To present value the deemed April 15th payments that come after the closing agreement date back to the closing agreement date, use the applicable short-term, mid-term, or long-term AFR. The short-term AFR applies for the first three deemed April 15th payments after the closing agreement date, the mid-term for the next three, and the long-term for those that follow. (For the present and future value mechanics, skip down to Section 4.81.6.5.3.9 of the IRM, which is confusingly titled “Computation of Present Value,” but really contains the rules for both present and future values.)

For the Luddites among you who don’t trust Excel, remember that the equation is:

Step 5 – Add up the Closing Agreement Date Values from Step 4. If you’ve made it this far, this step should be easy enough.

By tweaking the variables that we discussed above, an issuer or conduit borrower can see what its taxpayer exposure would be under a variety of factual situations that could arise under VCAP.

One closing note – much of the discussion above relates to the Internal Revenue Manual, a tome so hefty that it makes the Treasury Regulations look like a Batman comic book. Have you tried the “Helpful Links” button on the left column of the blog? There’s a specific link to the Internal Revenue Manual provisions that relate to tax-advantaged bonds down towards the bottom. We periodically add links that you might find helpful here, so check back often. If you have any items that you struggle to find that would be helpful here, let us know, and we’ll add them.